Summary

It’s easy to put your unwanted gift cards to good use by selling for cash, swapping for alternative cards or donating remaining balances to a good cause. See how some of the most popular gift card exchange sites stack up.

The content on this page is accurate as of the posting date; however, some of our partner offers may have expired. Please review our list of best credit cards, or use our CardMatch™ tool to find cards matched to your needs.

If you’ve got a stash of old gift cards crowding your wallet, you’re not alone. Although gift cards make for great last-minute presents and frequently pop up as a redemption option with rewards credit cards, they often end up forgotten or only half-used.

Indeed, a recent survey from Bankrate found that U.S. adults have more than $20 billion in unused gift cards and store credits, with the average person holding onto around $167 in unredeemed funds.

The good news is that instead of letting your gift cards go to waste, you can trade them in for cash, exchange them for more useful cards or donate them to charity, usually in just a few clicks.

How to turn gift cards into cash

If you’re looking to sell gift cards at a discounted price, you shouldn’t have much trouble finding a buyer. According to the National Retail Federation, gift cards have been the most popular item on consumer wish lists for 13 straight years, with 59% of those surveyed requesting gift cards as holiday presents in 2019.

While selling gift cards for cash won’t get you face value for your gift card, having this option could certainly come in handy if you’re short on cash or suspect the retailer that issued the card is headed for bankruptcy. After all, if a store shutters completely, your gift card could lose all its value.

Selling and exchanging gift cards through CardCash

CardCash.com buys gift cards directly from consumers, offering up to 92% cash back for your unwanted gift cards. Catering to the ease of digital exchanges, CardCash operates exclusively online.

While gift card prices fluctuate based on supply and demand, we found that many of the cards we tested fetched a decent value on CardCash. For example, when we checked, a $100 Best Buy gift card was valued at $86 and a $100 Walmart gift card was valued at $88. Of course, your experience may vary.

Additionally, CardCash features a robust list of accepted gift cards. Along with popular options such as Target and Walmart, you can sell gift cards from places like 7-Eleven, Costco, Starbucks and Uber Eats.

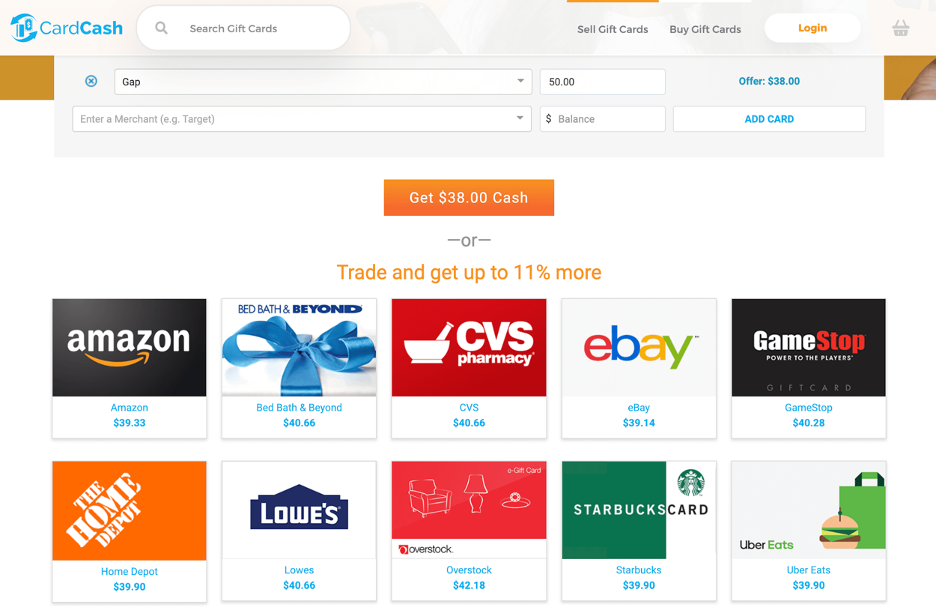

Selling gift cards at CardCash is easy: Simply enter a merchant and card balance, and you can see your offer instantly. You can also add multiple cards at once and see their total value. Only gift cards with a remaining balance of $10 or more are eligible.

Once you’ve selected your desired payment method – via check in the mail, ACH deposit or PayPal Express Checkout – enter your gift card number and PIN.

If you’d rather exchange your gift card for other store options, CardCash is one of your best bets. Indeed, the site offers up to 11% more value for your cards if you trade the gift card rather than sell it.

That said, the site’s selection of alternatives is limited. Currently, you can choose to exchange your gift card for a card at Amazon, Bed Bath & Beyond, CVS Pharmacy, eBay, GameStop, The Home Depot, Lowe’s, Overstock, Starbucks or Uber Eats.

Selling gift cards through Raise

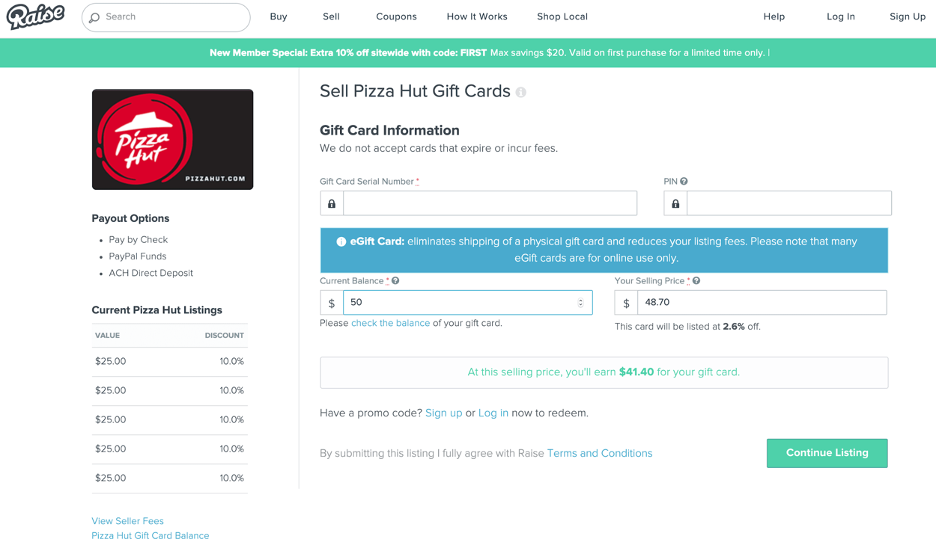

Unlike CardCash, Raise.com does not buy gift cards directly from consumers. Instead, Raise hosts an online marketplace where you can list your gift cards for sale or buy from other independent sellers.

Raise does not charge an upfront fee for hosting your gift card listing. Instead, if your card sells, the site deducts a 15% fee (plus $2.75 or 1% of the value of the physical card for shipping) from your final sale price and forwards you the rest. Raise also handles the actual transaction process, so you won’t need to deal directly with buyers. Simply list your cards and ship any physical cards once sold. You can receive payment via check in the mail, PayPal or ACH deposit.

Raise is also unique in letting you set your own price for your gift cards. In theory, this could allow you to squeeze a bit more value out of your cards – but there’s also no guarantee they will sell. CardCash, on the other hand, makes you a guaranteed offer you can take or leave.

For reference, Raise includes a suggested selling price and the discount offered by current card listings when you upload your gift card for sale. You’ll also see how much you’ll earn with Raise’s 15% fee factored in.

Raise’s suggested sale price is typically higher than the offers available at CardCash. But when you take Raise’s 15% fee into account, the difference is negligible.

For example, Raise suggested we list a $100 Walmart gift card for $99.13. With the 15% fee deducted, we stood to exchange the gift card for $84.26, compared to $88 at CardCash.

Are CardCash and Raise legitimate sites?

Yes, both are legitimate businesses and should offer more security than you’ll find selling gift cards yourself on a site like eBay or Craigslist. That said, each has faced its share of customer complaints and neither are accredited with the Better Business Bureau, so be aware.

CardCash’s BBB profile also notes a number of complaints, mostly from customers who had bought gift cards on the site and then had their card balances disappear after the site’s 45-day guarantee expired.

Raise’s customer service rating averages around 1 star on the Better Business Bureau site and 2 stars at Trustpilot. Like CardCash, most of Raise’s complaints relate to issues with buying gift cards, with some customers alleging the site performed a hard pull on their credit report.

We’ve reached out to both companies for comment on their customer service reputation and are awaiting comment.

How to donate gift cards

Another great way to use your unwanted or low-balance gift cards is to donate them to charity, either directly or via a site like GiftCards4Change.

GiftCards4Change’s mission is to “collect, combine and liquidate gift cards through relationships with merchants, corporate sponsorship programs and third-party vendors to maximize the value of your remaining gift card balance.”

This means that even if you’ve used a portion of your gift card, you can donate what’s left of the gift card to GiftCards4Change to make a difference in areas like poverty assistance, education advancement, human trafficking and homelessness. As the site notes, “In some cases, we are able to double [or] triple the value of your donated card with donor match programs and local community initiatives.”

GiftCards4Change sells gift cards as well, with 100% of your purchase going directly to charity.

CardCash has also occasionally offered users the option of donating gift cards to charity instead of exchanging the gift card for cash. The site partnered with Charity on Top for a donation program during Hurricane Harvey and is currently working with St. Jude Children’s Research Hospital.

Unfortunately, donating via CardCash won’t yield the full value of your gift card – for example, a $100 Walmart gift card would get St. Jude’s $88 – so it may be worth contacting a local charity directly about donating unwanted cards instead.

Whichever route you take, be sure to get a receipt for the value of the gift card so that you can claim your donation as a tax deduction.

Bottom line

Whether you decide to sell them for cash, swap for an alternative, or pass on the remaining value to those in need, your old, unwanted or low-balance gift cards can be put to good use.

You may only get back 70%–80% of your card’s value, but that’s certainly better than letting them go to waste.

Editorial Disclaimer

The editorial content on this page is based solely on the objective assessment of our writers and is not driven by advertising dollars. It has not been provided or commissioned by the credit card issuers. However, we may receive compensation when you click on links to products from our partners.

Essential reads,

delivered straight to your inbox

Stay up-to-date on the latest credit card news 一 from product reviews to credit advice 一 with our newsletter in your inbox twice a week.