Summary

Google Pay has added new features, introducing rewards, targeted deals and financial insights. Here’s everything you need to know about using the app, as well as security, privacy, payment options and fees.

The content on this page is accurate as of the posting date; however, some of our partner offers may have expired. Please review our list of best credit cards, or use our CardMatch™ tool to find cards matched to your needs.

When someone says “Google,” you probably think “web search.” But the tech giant wants you to think about peer-to-peer payments and shopping, too.

The latest incarnation of Google Pay combines a mobile wallet with a peer-to-peer payment system – and adds access to deals and budgeting insights on top.

Depending on how you set it up, you can use it to shop with retailers and e-tailers, send and receive money among friends and family, split a check at the table, earn cash back, track your budget – or all of the above.

Want to learn more? Here are some of the basics on Google Pay.

See related: 3 major mobile payment security risks, and how to avoid them

A guide to Google Pay

- What is Google Pay?

- How do you set up Google Pay?

- How does Google Pay work?

- Is the money on Google Pay protected against loss, fraud and theft?

- How much does it cost to use Google Pay?

- What’s the difference between Google Pay and Google Wallet?

- Are Google Pay transactions public?

- How can you protect yourself when using Google Pay?

- Can users earn credit card rewards and loyalty points through Google Pay?

- Does Google Pay offer its own cards?

- Do I need extra security when using Google Pay?

What is Google Pay?

“Google Pay is an easy way for anyone with a Google account – Gmail, Chrome, YouTube, etc. – to be able to pay online and in stores and also send money to friends and family,” says Gerardo Capiel, product management director for Google Pay.

But after the last relaunch, Google Pay is much more than that. The new version of the app comes with three new tabs: “Pay,” “Explore” and “Insights.”

In “Pay,” you can get access to peer-to-peer payments and your transaction history using tap-to-pay. In “Explore,” you’ll find deals and discounts based on where you shop. “Insights” provides you with an overview of your finances similar to Mint and other budgeting apps.

In 2021, Google Pay is also planning to add banking features in partnership with Citi and Stanford Federal Credit Union. The feature will be called “Plex Account” and will allow users to manage their checking and savings accounts right in Google Pay. Currently, you can join a waitlist for early access in the app.

How do you set up Google Pay?

Go online to Google Pay or download the app – available for both Android and iPhone devices. Note that starting January 2021, you won’t be able to use the browser version to send or receive money, and these features will only be available on the app.

Once you’ve downloaded the app, create an account.

- Connect your Google email account.

- Supply your phone number and verify it – the verification code will be sent to you via text.

- Set a few privacy settings, including whether you want to allow people to identify your account by your phone number or let Google Pay use your data to offer you rewards and personalized offers (more on that later).

- Complete verification. To be able to send money, you’ll need to set up your Google Pay balance by providing your first and last name, address, date of birth and last four digits of your SSN.

- Then you link your Google Pay account to a bank account, credit card or debit card.

One caveat: Your choice of financial tool will determine what you can (and can’t) do with Google Pay.

- Debit card: You can use the account to shop online or in stores, as well as send and receive money from individuals.

- Bank account: You can only send or receive money from individuals. No shopping allowed.

- Credit card: You can shop with merchants online or at brick-and-mortar locations, but you can’t send or receive money from individuals.

The type of financial tool you use with any brand of peer-to-peer payment account “makes a big difference in terms of your rights with fraud and disputing payments,” says John Breyault, vice president of public policy, telecommunications, and fraud for the National Consumers League.

And if you link your Google Pay account to a debit card, “it may be tough to dispute,” he adds.

See related: Debit cards versus credit cards: Know the differences

How does Google Pay work?

With Google Pay, you can do much more than just pay and receive money. Let’s explore the app’s three tabs and see what they can offer.

Explore

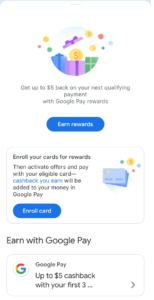

The first tab is “Explore,” where you can get access to special offers and Google Pay rewards. To take advantage of offers, you’ll need to connect your eligible card (note that Discover cards are currently not eligible), so that Google can provide you with offers based on your transaction history.

Once your card is connected, you’ll see offers ranging from popular deals to cash back at stores near you. You’ll need to activate the offer and make a qualifying purchase with your enrolled card to earn rewards. The cash back you earn will be added to your Google Pay balance.

If you’re not sure if the potential rewards justify letting Google access your transactional data, the app offers a three-month trial of the feature. After that period is over, you’ll be prompted if you’d like to continue using the service.

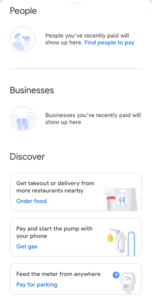

Pay

In the “Pay” tab, you’ll see your payment history, including people and businesses you’ve recently paid. This is also where you can find your friends to send them money.

The “Discover” section of the tab shows you how you can use Google Pay locally – for example, you can order food within the app, pay for gas when you’re at the pump and feed the parking meter from anywhere.

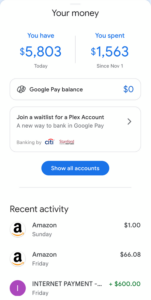

Insights

“Insights” offers you a look into your spending when you connect your bank accounts through Plaid. Additionally, you can opt in to share data from your Gmail and Google Photos accounts, which Google Pay will scan for receipts.

While the overview might not be as detailed as in other budgeting apps, the ability to search transactions by terms, such as “Chinese restaurants” or “shoes” sets this feature apart. You can also combine the terms to narrow down the results.

At the top of your “Insights” screen, you’ll also see blue icons representing quick summaries of useful information, such as large transactions, upcoming bills and more.

Is money protected against loss, fraud and theft?

When you use Google Pay, the other party or merchant doesn’t receive your actual credit or debit card number, says Capiel. Instead, they receive a one-time-use number that works only for the transaction. Known as tokenization, it can protect your card if the merchant or payee is breached.

When it comes to regulations that protect you from fraud and theft, Google Pay is the conduit through which you use a bank account, debit card, credit card or PayPal account. So, whatever protections are in place for those financial instruments still apply if you access them through Google Pay.

- Consider how you want to use your Google Pay account, as well as what payment options you feel most secure using online.

- Credit cards often offer $0 liability in cases of theft or fraud. They also give you dispute rights.

- With debit cards and bank accounts, the legal liability for theft or fraud is $50 – if you report the loss within two days of discovery. But you may be without that money until the bank investigates. And if the bank decides you’re at fault, you take the loss.

- When you use a peer-to-peer payment service, there are no guaranteed ways to retrieve money once it’s sent. So, you need to carefully vet the recipient’s address or phone number before the transaction, as well as proofread every part of the transaction several times before you hit send.

Google Pay’s app “does warn you when you’re sending to someone who’s not in your contact list,” says Capiel.

In addition, the Google Pay service shows the sender the final sending amount so they can verify or reject it.

And, “depending on how the recipient has it set up to receive the money, you may have some time to cancel the send,” says Capiel.

If those solutions don’t work, and you’ve sent money to the wrong person or in the incorrect amount, Google Pay urges users to call its customer service center and their bank, he says.

See related: Venmo Guide: How to send, receive money using Venmo

How much does it cost to use Google Pay?

Google Pay charges a transfer fee of 1.5% (minimum of 31 cents) when you’re transferring funds available in your Google Pay balance to a debit card. Paying the fee makes the transfer instant, and the funds will be available immediately. Alternatively, you can cash out this balance to a linked bank account at any time without a fee if desired. This process can take up to 5 business days.

All other Google Pay features are free to use.

How quickly does the other party receive money sent through Google Pay?

That depends on which payment device you’ve linked to your account.

- If you’re using a debit card, typically “it’s within minutes,” says Capiel.

- If you’re your Google Pay balance, the recipient will also get the money almost right away.

- With a bank account, “it really depends on the bank,” he says. “We typically say it takes one or two days.”

- With a credit card or PayPal, you can’t send money to an individual through Google Pay.

See related: Is PayPal safe? 10 security tips to protect yourself

What’s the difference between Google Pay and Google Wallet?

What used to be called Google Wallet has been combined with Android Pay – and is now called Google Pay.

See related: Guide to mobile wallets: Samsung Pay, Apple Pay, Google Pay

Are Google Pay transactions public?

No. Unlike Venmo, Google Pay doesn’t have a social media component. Only the sender and receiver (and their banks or credit card issuers), know about the transaction.

How can you protect yourself when using Google Pay?

When it comes to dealing with individuals and peer-to-peer payments, you only want to send money to people you know and trust.

Scammers are already altering old cons to fit new technology, says Alexandra Hamilton, digital communications coordinator for the Identity Theft Resource Center.

Always independently verify any request for payment. And never use a peer-to-peer service to pay for goods you haven’t yet received.

“Be really careful who you’re sending money to,” says Breyault.

Can users earn credit card rewards and loyalty points through Google Pay?

Yes. If you link your Google Pay account to a rewards credit card, you’ll still earn those rewards on top of the cash back you may be earning within the app.

As far as the credit card and merchant are concerned, you’re paying with your credit card, so you get any rewards or cash back that card awards for purchases from that merchant, says Capiel.

So when you use Google Pay to make your purchase, your loyalty rewards are automatically added to your account.

“They can add many other types of loyalty cards,” Capiel says. “It’s another great way to save money.”

That said, you might want to read the fine print on special promotions run by your credit card when it comes to paying with a mobile wallet.

Does Google Pay offer its own cards?

Not in the U.S. However, in some other countries, Google Pay uses a contactless card for real-world transactions instead of a phone app.

Do I need extra security when using Google Pay?

If your phone is now your wallet, you need wallet-level security.

A few easy moves:

- Make sure your phone is password protected, whether you use a PIN, a fingerprint or password, says Hamilton. And make sure it’s a unique PIN or password – not the one you use everywhere else.

- Also, shorten the length of time your phone has to idle before it locks, says Hamilton. That way, if you leave it somewhere and someone grabs it, you lessen the amount of time they have to rob you.

- When you want to use Google Pay, “typically, you log in with email address,” says Capiel. He also urges users to take advantage of two-factor authentication – with a phone number and email address.

- Use anti-malware and antivirus protection on devices and keep it updated, says Breyault. And employ two-factor authentication not just with any peer-to-peer payment system itself, but also with any email address you associate with that service.

- Contact your card issuer to add an extra PIN or two-factor authentication on the financial account you’ll use for P2P payments and within mobile wallets. And ask what security measures it can offer.

See related: How to protect your cards and accounts online

Editorial Disclaimer

The editorial content on this page is based solely on the objective assessment of our writers and is not driven by advertising dollars. It has not been provided or commissioned by the credit card issuers. However, we may receive compensation when you click on links to products from our partners.

Essential reads,

delivered straight to your inbox

Stay up-to-date on the latest credit card news 一 from product reviews to credit advice 一 with our newsletter in your inbox twice a week.